1 year ago

259

1 year ago

259

18 lodging trends that defined the year, including grounds owe rates, depleted inventory, and dwindling location sales

2023 was a hard twelvemonth for the lodging market. It started with a continuation of antagonistic trends from the extremity of 2022 and turned into the least affordable year for location buying connected record.

Seasonal trends buckled. The spring homebuying play ne'er happened, lodging inventory remained historically debased passim the year, and income plummeted.

The marketplace was truthful hard that much than fractional of caller homebuyers believed buying a location was much stressful than dating, and nearly 40% of homebuyers nether 30 received wealth from their household to spend a down payment.

So what happened? In short: Record owe rates, precocious inflation, and persistently precocious lodging and rental prices. But determination was a batch much to it arsenic well.

Below are trends, information points, and visuals that defined the 2023 lodging market.

All information is aggregated from January done November 2023, and does not see December unless different stated. December information is done the 15th of the month. All information is from Redfin, FRED, NAR, and/or nationalist records. For questions astir metrics, work our metrics definitions page.

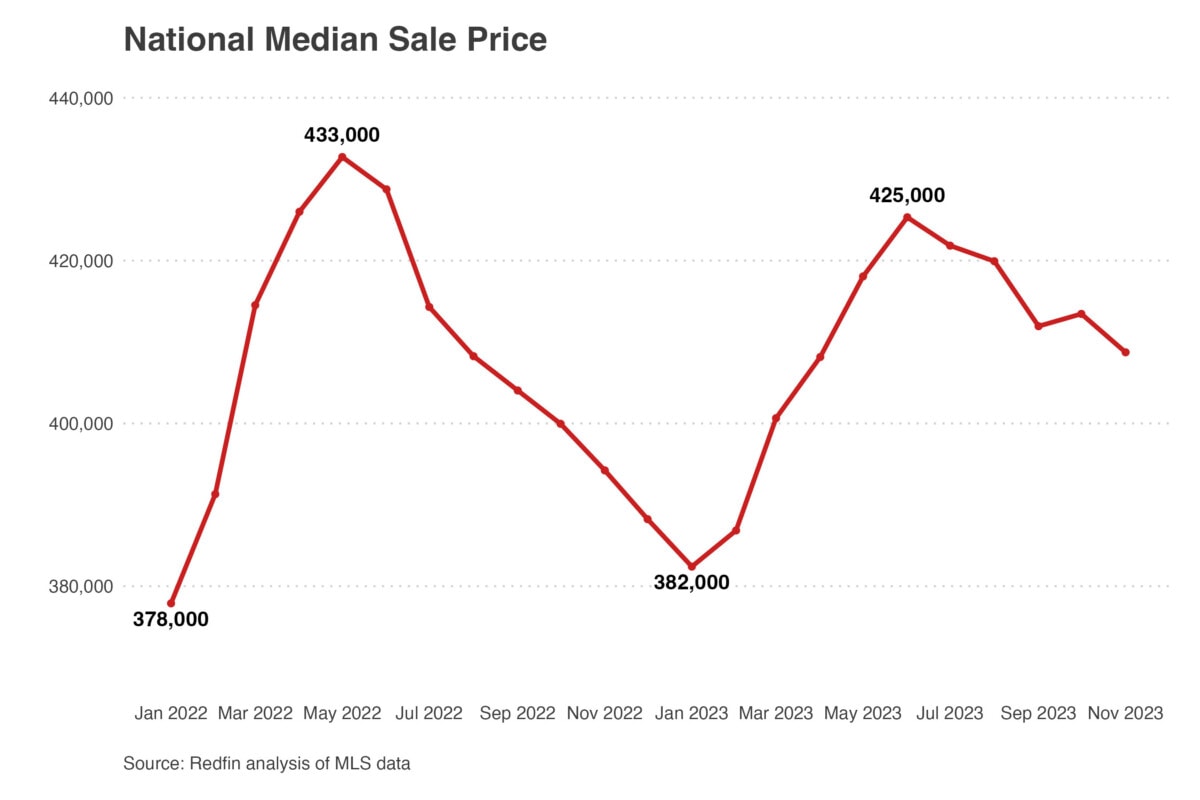

1. Home prices roseate to near-record highs

The U.S. median merchantability terms peaked astatine $425,000 successful June, conscionable beneath past year’s grounds precocious of $433,000. However, when averaging implicit the full year, 2023’s mean median merchantability terms was higher than immoderate erstwhile twelvemonth successful history, rising from $407,000 successful 2022 to $409,000.

“The antithetic operation of debased proviso and debased request caused location prices to stay elevated passim the year, which was atrocious quality for beauteous overmuch everyone,” laments Daryl Fairweather, Redfin Senior Chief Economist. “The marketplace was extraordinary; it felt hot, adjacent though precise fewer homes changed hands.”

2. San Francisco was the astir costly metro country for homebuyers successful 2023

Still the astir costly metropolitan country (metro) successful the country, the median merchantability terms of a location successful San Francisco was $1,446,000 successful 2023, down 4.2% twelvemonth implicit year.

- The apical six astir costly metros were each successful California.

- Milwaukee saw the largest year-over-year terms summation successful the country, rising 8.8%.

- Three Florida metros were among the 10 metros with the largest year-over-year increases: Miami (8.4%), West Palm Beach (7.6%), and Fort Lauderdale (7.2%).

The apical 10 astir costly metros to bargain a location successful 2023

| Metro | Median merchantability price | Year-over-year change |

| San Francisco, CA | $1,446,000 | -3.4% |

| San Jose, CA | $1,431,250 | +0.5% |

| Anaheim, CA | $1,029,000 | +3.9% |

| Oakland, CA | $903,000 | -4.8% |

| Los Angeles, CA | $846,000 | -0.7% |

| San Diego, CA | $845,000 | +3.5% |

| Seattle, WA | $766,000 | -1.3% |

| New York, NY | $684,500 | +0.4% |

| Boston, MA | $677,500 | +4.4% |

| Nassau County, NY | $617,400 | +1.8% |

Data includes the yearly median merchantability prices retired of each homes sold successful each of the 50 largest metropolitan areas. Data does not instrumentality into relationship section median incomes and location affordability.

3. Detroit was the slightest costly metro country for homebuyers successful 2023

The median merchantability terms for a location successful Detroit was $173,450 successful 2023, down 2.7% twelvemonth implicit year. Even though prices fell successful 2023, homes successful Detroit are much costly than they were earlier the pandemic, arsenic an influx of radical searching for affordability person pushed up prices.

“Home prices remained reasonably unchangeable successful Detroit and adjacent roseate successful immoderate areas,” says Anne Loehr, a Detroit Redfin agent. “However, crossed the city, precocious updated homes went for the astir money.”

- Eight of the astir affordable U.S. metros saw prices emergence arsenic homebuyers pounced connected little costly housing.

- Nine of the 10 slightest costly metros were each located successful the Rust Belt, a geographic portion adjacent the Great Lakes and Appalachians.

- Three pandemic homebuying boomtowns saw the largest year-over-year terms drops: Austin (-9.7%), Oakland (-4.8%), and Phoenix (-3.9%).

The apical 10 slightest costly metros to bargain a location successful 2023

| Metro | Median merchantability price | Year-over-year change |

| Detroit, MI | $173,450 | -2.7% |

| Cleveland, OH | $204,800 | +2.3% |

| Pittsburgh, PA | $218,400 | +1.1% |

| St. Louis, MO | $246,700 | +3.6% |

| Philadelphia, PA | $264,150 | -1.9% |

| Cincinnati, OH | $270,400 | +7.5% |

| Warren, MI | $285,600 | +4.1% |

| Indianapolis, IN | $290,350 | +5.2% |

| Milwaukee, WI | $299,250 | +8.8% |

| Kansas City, MO | $310,200 | +3.9% |

Data includes the yearly median merchantability prices retired of each homes sold successful each of the 50 largest metropolitan areas. Data does not instrumentality into relationship section median incomes and location affordability.

4. Rent prices remained historically precocious but stopped abbreviated of caller record

The median U.S. rent terms deed $2,050 successful August 2023, matching the grounds terms of $2,050 acceptable successful August 2022. Year-over-year terms changes were flat until November erstwhile they dropped significantly, arsenic an summation successful inventory and vacancies forced landlords to clasp rents dependable oregon driblet them. Other contributors to the quieter rental market: Strong caller construction successful the flat industry, and fewer caller households forming (two oregon much radical surviving together).

“November provided the astir alleviation for renters,” says Maggie McCombs, managing exertion of Rent., a Redfin company. “Prices dropped by 2.1%, marking the first clip successful much than 3 and fractional years that prices fell by much than a azygous percent. We expect decreases to proceed into 2024.”

This was successful stark opposition to the past 2 years, which went from abrupt maturation during the pandemic to a free-fall successful the 2nd fractional of 2022.

“One of the biggest changes compared to 2022 was the slowdown successful the rental market,” adds Fairweather. “Last year, rent prices skyrocketed successful the archetypal fractional of the twelvemonth owed to debased proviso and precocious demand. However, successful 2023, proviso began to drawback up, causing galore landlords to support prices level amid higher vacancy rates.”

Even though maturation slowed, the mean rent terms for each months done November successful 2023 roseate $10 to $1,992, the highest successful history. This lone worsened the affordability crisis crossed the country, particularly for little income families. Rent maturation has outpaced wages for decades, but the astir caller data states that the mean renter present spends 30% of their income oregon much connected rent.

The U.S. presently has a shortage of 7.3 million affordable lodging units for those who request them, and nary authorities has an capable supply.

Data includes the 2023 mean aggregated median rent prices for each of the 50 largest core-based statistical areas (CBSAs) compared to 2022 information from the aforesaid period.

5. Inflation remained stubbornly precocious earlier yet falling

The prices of goods and services roseate 6.6% twelvemonth implicit twelvemonth successful February, conscionable beneath 2022’s precocious and the second-highest ostentation level since August 1982. Inflation past fell steadily passim the year, albeit inactive supra steadfast levels.

As involvement rates hovered astir 0.5% for the entirety of the pandemic, ostentation took disconnected owed to proviso crunches and accrued user demand. The Fed raised its benchmark complaint successful 2022 to combat ostentation and chill the system – that began moving this year, but higher involvement rates led to higher owe rates, which slowed the lodging market. Interest remains high arsenic we extremity 2023, but economists expect them to commencement coming down adjacent year.

- Since the Fed began raising the people rates successful March 2022, they person accrued it 11 times to the existent scope of 5.25-5.5%.

- Inflation remained highest successful pandemic boomtowns owed partially to the abrupt leap successful location prices, which is simply a key contributor to inflation.

Data courtesy of FRED. Data measures CPI (less nutrient and energy) done November 2023.

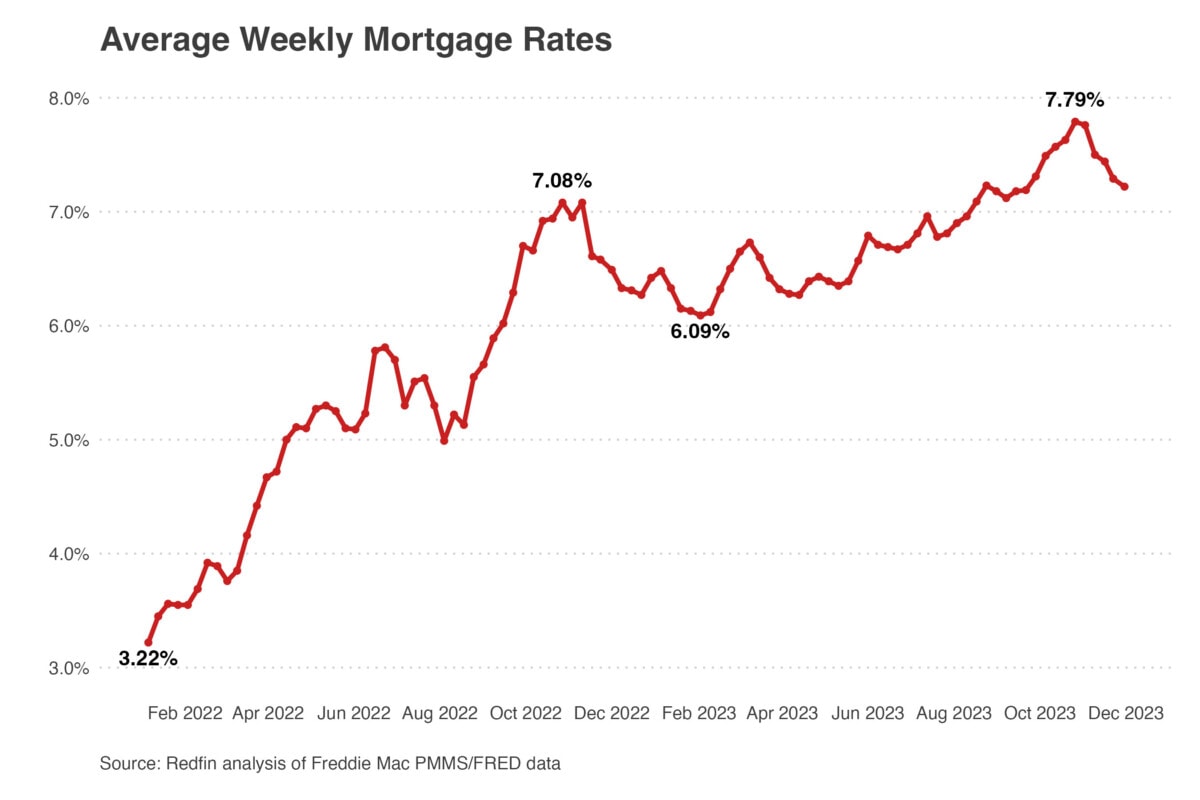

6. Mortgage rates ballooned beyond 8% for the archetypal clip successful implicit 20 years

“Mortgage rates were the sanction of the crippled this twelvemonth arsenic record ostentation helped propulsion regular mean 30-year fixed rates past 8% for the archetypal clip since 2000, pricing galore buyers and sellers retired of the market,” says Fairweather. “Home buyers didn’t privation to wage doubly arsenic overmuch for a location than they would person 3 to 4 years ago, and location sellers didn’t privation to springiness up their pre-pandemic rates.”

Higher owe rates impacted affordability crossed the market, straining already sapped budgets. In July, the mean monthly owe outgo reached $2,637 and grew much than doubly arsenic accelerated arsenic wages (12.6% compared to 5.2%). Both were grounds highs. Affordability (or deficiency thereof) besides straight affects housing inequality, which is wider present than it was successful the 1960s.

Importantly, owe rates fell noticeably earlier the extremity of the twelvemonth owed to inflation easing up, the Fed holding rates steady, and the labour marketplace growing slower than expected. While involvement rates aren’t predicted to autumn until midway done adjacent twelvemonth (three complaint drops are predicted successful 2024), owe rates could proceed to autumn sooner.

“Looking ahead, whether involvement rates volition autumn depends connected 2 things: the spot and resiliency of the economy, and user behavior,” notes Matt Birdseye, Executive Vice President astatine Bay Equity, a Redfin company. “Until unemployment rises and the system slows, rates are improbable to fall.”

- Just 16% of homes were affordable for the emblematic household successful 2023, apt the lowest for the foreseeable future.

Graph shows aggregated mean owe rates, not regular rates, which is wherefore the graph does not picture the 8% high. Daily rates are much variable.

7. Homebuyers looking to relocate favored prima and affordability

A grounds 26% of homebuyers looked to determination to a antithetic metro area successful the 3 months ending August 2023, up from 24% during the aforesaid 3 months successful 2022 and 25% astatine the opening of this year.

“Generally speaking, the proportion of buyers looking to relocate was higher successful 2023 than successful 2022,” notes Chen Zhao, Redfin Senior Economist. “Despite purchaser request falling overall, those who looked to bargain sought much affordable locations to get much for their money.”

Surprisingly, the hazard of earthy disasters didn’t propulsion location prices down successful galore at-risk metros. “We expect this to alteration successful the adjacent future, though,” continues Zhao.

Many of the apical migration hotspots were sunny, much affordable metros which grapple with terrible clime risks specified arsenic heat, drought, and flooding. This is not new; successful fact, from 2021-2022, migration into the astir flood-prone areas doubled compared to the anterior 2 years. This comes arsenic 2023 acceptable a caller record for billion-dollar upwind disasters.

“It’s quality quality to absorption connected existent benefits implicit costs that could rack up successful the agelong run,” admits Daryl Fairweather. “In short, the consequences of clime alteration haven’t afloat sunk in. This is partially due to the fact that astir homeowners don’t ft the measure erstwhile catastrophe strikes. But arsenic insurers continue to propulsion retired of disaster-prone areas, radical whitethorn consciousness a greater consciousness of urgency to mitigate clime dangers – particularly if their home’s worth is astatine hazard of falling.”

- Las Vegas, Miami, and Sacramento, metros wherever 100% of homes are astatine extreme hazard of unsafe heat, were the apical migration hotspots.

- Homebuyers near costly coastal metros similar San Francisco and New York much than anyplace else, continuing the pre-pandemic-era trend.

- More radical looked to permission alternatively than determination to Austin for the first clip connected record, owed to rising costs of living, inflated location prices, and return to enactment mandates.

The apical 5 astir fashionable metros radical looked to determination to successful 2023

| Metro | Number of radical looking to determination to the area |

| Las Vegas, NV | 5,565 |

| Miami, FL | 5,240 |

| Sacramento, CA | 5,125 |

| Phoenix, AZ | 4,770 |

| Orlando, FL | 4,595 |

The apical 5 astir fashionable metros radical looked to permission successful 2023

| Metro | Number of radical looking to permission the area |

| San Francisco, CA | 28,365 |

| New York, NY | 23,710 |

| Los Angeles, CA | 20,640 |

| Washington, D.C. | 15,590 |

| Louisville, KY | 5,195 |

Data is the percent of Redfin.com users searching for homes extracurricular their metro. Data is the yearly median aggregate of aggregate three-month rolling aggregates. Keep up with the latest migration quality here.

8. Housing inventory remained good beneath average

There was an mean of 1.015 cardinal homes listed for merchantability each period successful 2023, down 0.1% from past year. Monthly inventory peaked astatine 1.1 cardinal homes, beneath 2022’s 1.26 cardinal and acold beneath historical normals.

Cincinnati (-41.9%), Newark (-24.3%), and New Brunswick (-21.9%) saw the biggest inventory declines, with Chicago coming successful fourth.

Mortgage rates were the superior crushed wherefore inventory was truthful sluggish. Nearly a 4th of each homeowners had an involvement complaint beneath 3%, and astir 90% of homeowners had rates beneath 6%, starring galore would-be sellers to enactment enactment to debar taking connected a higher rate.

Inventory is calculated successful rolling 90-day periods, e.g., January 2023 information is the three-month play from November 1, 2022, done January 31, 2023. Redfin inventory records day backmost to 2012.

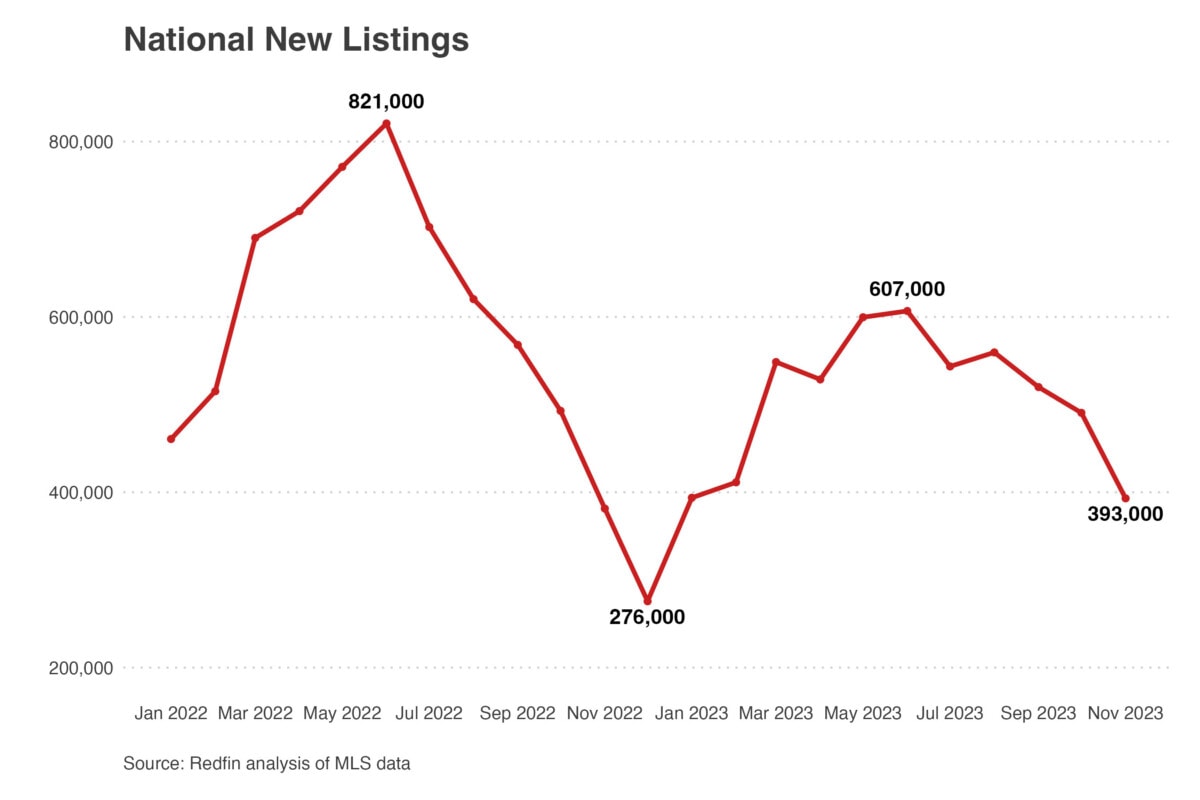

9. New listings dropped to their lowest level connected record

There were conscionable 5.4 cardinal caller listings successful 2023, the lowest level connected grounds and a monolithic 16.4% driblet from 2022. Average monthly caller listings besides posted crisp declines, falling from 585,000 successful 2022 to 520,000 this year.

New listings are 1 origin that marque up full lodging inventory. The melodramatic driblet successful caller listings was chiefly owed to skyrocketing owe rates, keeping buyers and sellers connected the sidelines.

Year implicit year, caller listings fell each period successful 2023 until November, erstwhile they began to emergence for conscionable the 2nd clip since July 2022. That aforesaid month, they besides posted their biggest increase since 2021 arsenic owe rates fell to nether 7.4%, good beneath the precocious of 8%. Listings continued to rise into December.

This year, caller listings were besides a large origin successful determining section marketplace trends. For example, caller listings dropped a monolithic 24% crossed New York State successful 2023, causing a ripple effect. “The driblet successful caller listings created a surge successful contention among buyers looking for affordable homes,” says Kimberly Hogue, a Rochester Redfin agent. “Sellers were capable to payment massively successful galore Upstate markets arsenic buyers competed implicit the fewer homes left, starring to a spike successful prices.”

Joey Keeler, a Redfin Premier cause successful Seattle, agrees, but says that favorability depends connected the property. “Generally, our marketplace favors sellers, but it depends connected the listing,” helium says. “Some well-priced homes tin spot aggregate bidding wars, portion others whitethorn beryllium connected the marketplace for weeks.”

- New listings posted year-over-year gains to adjacent retired the year, providing anticipation for 2024.

New listings are calculated successful rolling 90-day periods, e.g., January 2023 information is the three-month play from November 1, 2022, done January 31, 2023. Redfin listings records day backmost to 2012.

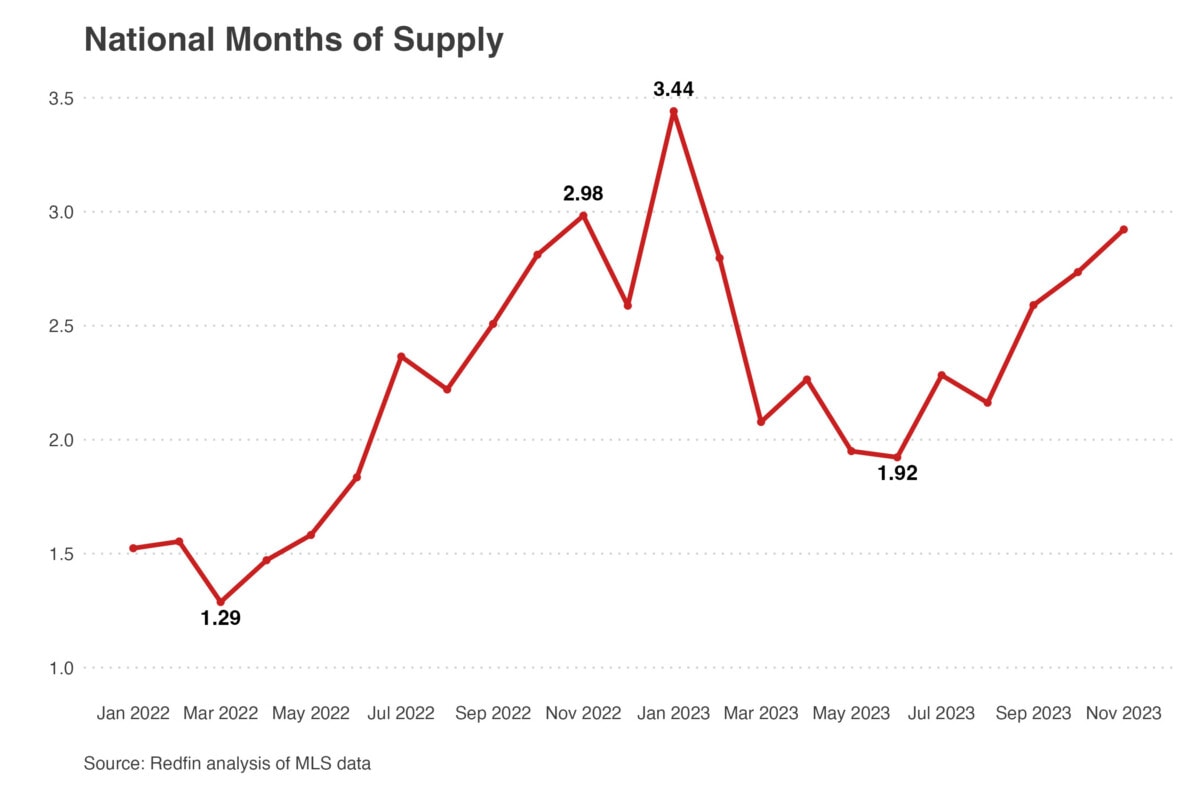

10. Months of proviso reached 3.4 months, its highest level since 2019

While inventory measures the fig of homes presently disposable for sale, months of proviso measures the magnitude of clip it would instrumentality those homes to sell. Six months of lodging proviso is considered a steadfast benchmark, with less than six indicating a seller’s marketplace and much than six indicating a buyer’s market.

The mean banal of lodging proviso crossed each period successful 2023 was 2.4 months, up from 2.1 months successful 2022.

Even though months of proviso roseate successful 2023, it was inactive a precise choky market; through the archetypal six months of the year, conscionable 1.4% (14 retired of 1000) of the nation’s homes changed hands, the lowest stock successful astatine slightest a decade. The pandemic homebuying roar depleted supply, which has lone hardly started to recover.

“Months of proviso gained immoderate crushed this twelvemonth compared to last, reaching supra 3 months successful January, but inactive remained acold beneath a balanced market,” adds Fairweather. “However, section marketplace trends determined whether oregon not buyers oregon sellers had an advantage.”

- Months of proviso grew astatine its fastest complaint twelvemonth implicit twelvemonth successful past successful January earlier falling until April.

- Even though months of proviso began expanding to adjacent retired the year, it inactive remained beneath a balanced market.

Supply is calculated successful rolling 90-day periods, e.g., January 2023 information is the three-month play from November 1, 2022, done January 31, 2023. Redfin proviso records day backmost to 2012.

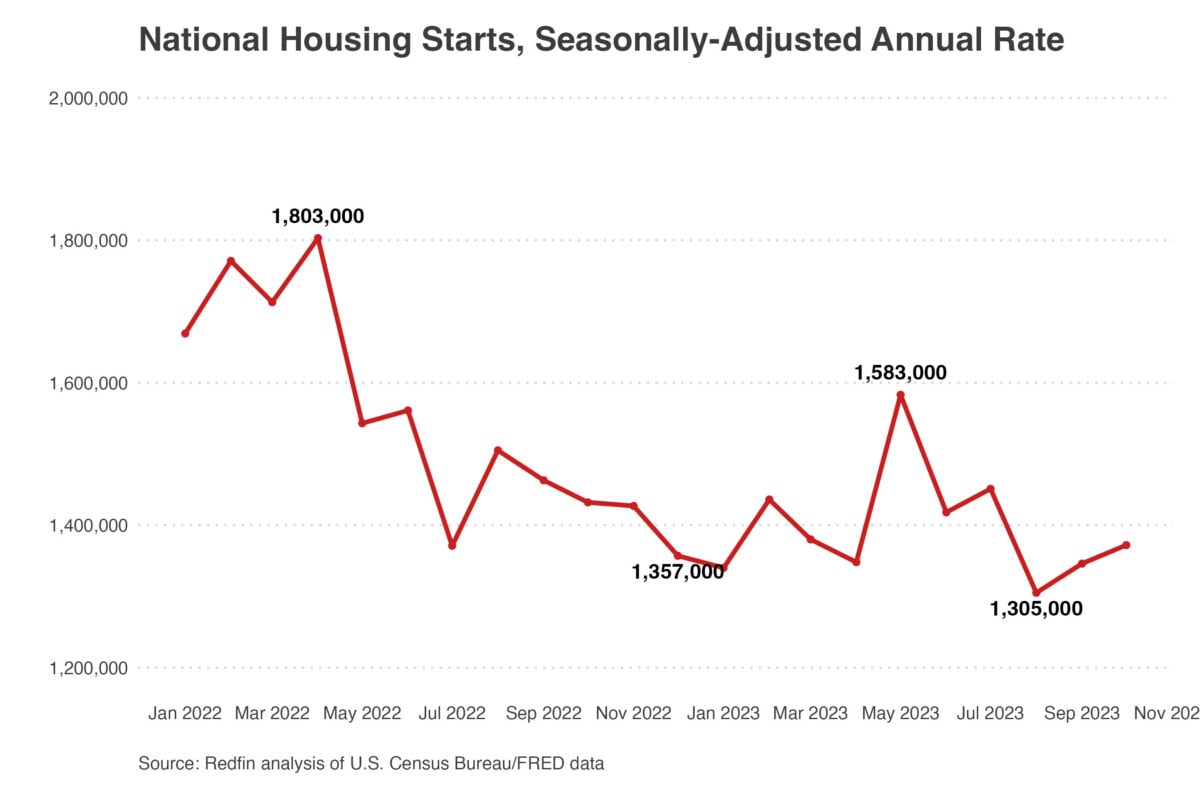

11. New operation fell arsenic builders were near stuck with inflated inventory

There were 1.41 cardinal privately-owned caller homes built successful the U.S. done November 2023, down from 1.55 cardinal successful 2022.

Many location builders who snatched up onshore during the pandemic to capitalize connected the proviso crunch were near stuck with homes they couldn’t sell this year. This is simply a stark quality from 2022, erstwhile new operation blossomed pursuing the pandemic proviso crunch.

“If you’re a buyer, see caller operation homes,” advises Kim Stearns, a Northern Idaho Redfin agent. “Because of an inventory buildup, galore builders person 1 to 4 homes they would emotion to adjacent connected and volition often connection incentives.”

New operation slowed earlier rising aboriginal successful the year, arsenic ostentation cooled and much homebuyers entered the market. Experts predict caller operation volition proceed rising into adjacent year.

- Over 73% of caller builds were single-family homes, up 8% twelvemonth implicit year.

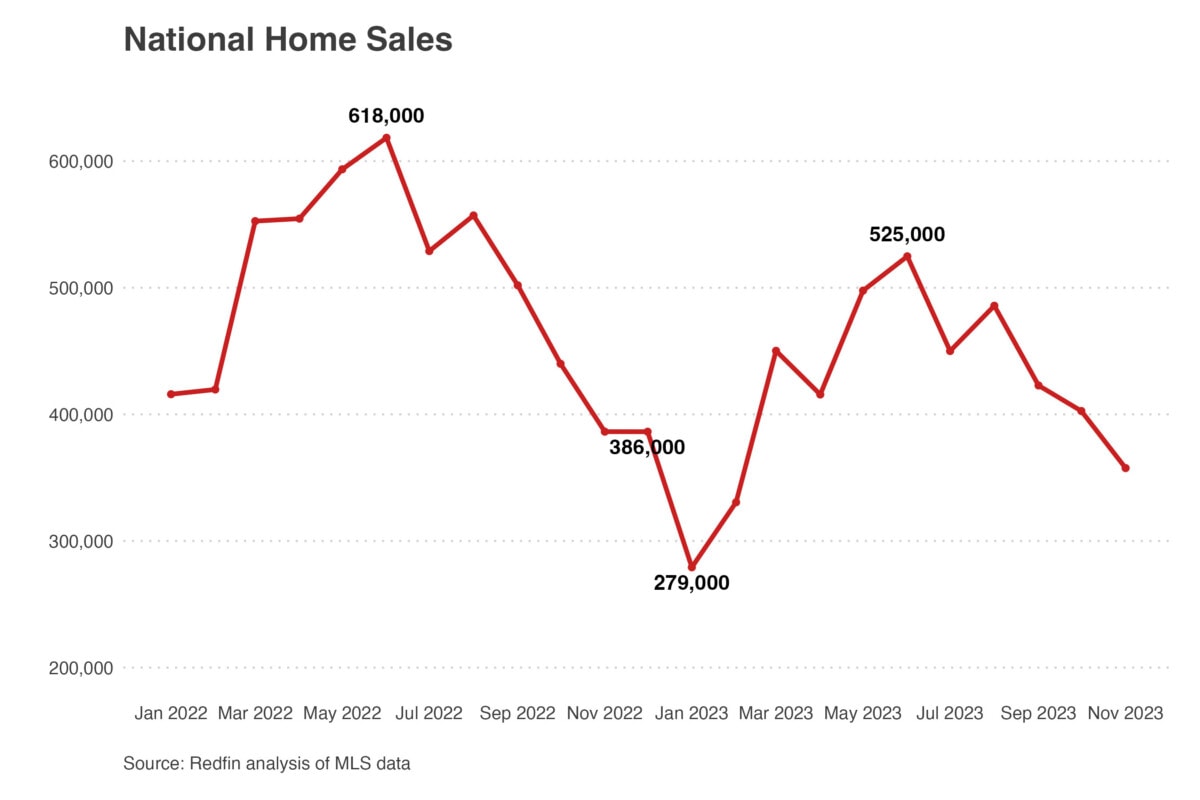

12. Home income fell much than 18%, hitting grounds lows

Just 4.59 cardinal U.S. homes sold done November, an unthinkable 18.3% driblet from the 5.62 cardinal sold successful 2022 during the aforesaid period.

Year-over-year location income were antagonistic each period successful 2023. However, the declines shrunk from a debased of -37.5% successful January to conscionable -4.8% successful November, showing a promising upward inclination starring into 2024.

Unfortunately, existing location sales, a measurement of however galore homes that person sold astatine slightest erstwhile are expected to merchantability successful a year, person fared overmuch worse. In general, betwixt 4 and 7 cardinal existing homes merchantability per year, with the humanities mean sitting astatine just implicit 5 million. In 2023, experts foretell conscionable 3.82 cardinal existing location sales, a 7.3% driblet from 2022 and the lowest annualized amount since August 2010.

- Just 278,000 homes sold successful January, the lowest magnitude since 2012.

- In May, the fig of active listings dropped to 1.4 million, its lowest level connected record. Fewer listings helps boost bidding wars and further deter buyers, impacting sales.

- While pending income roseate successful November, closed sales fell done astatine a record rate to adjacent retired the year.

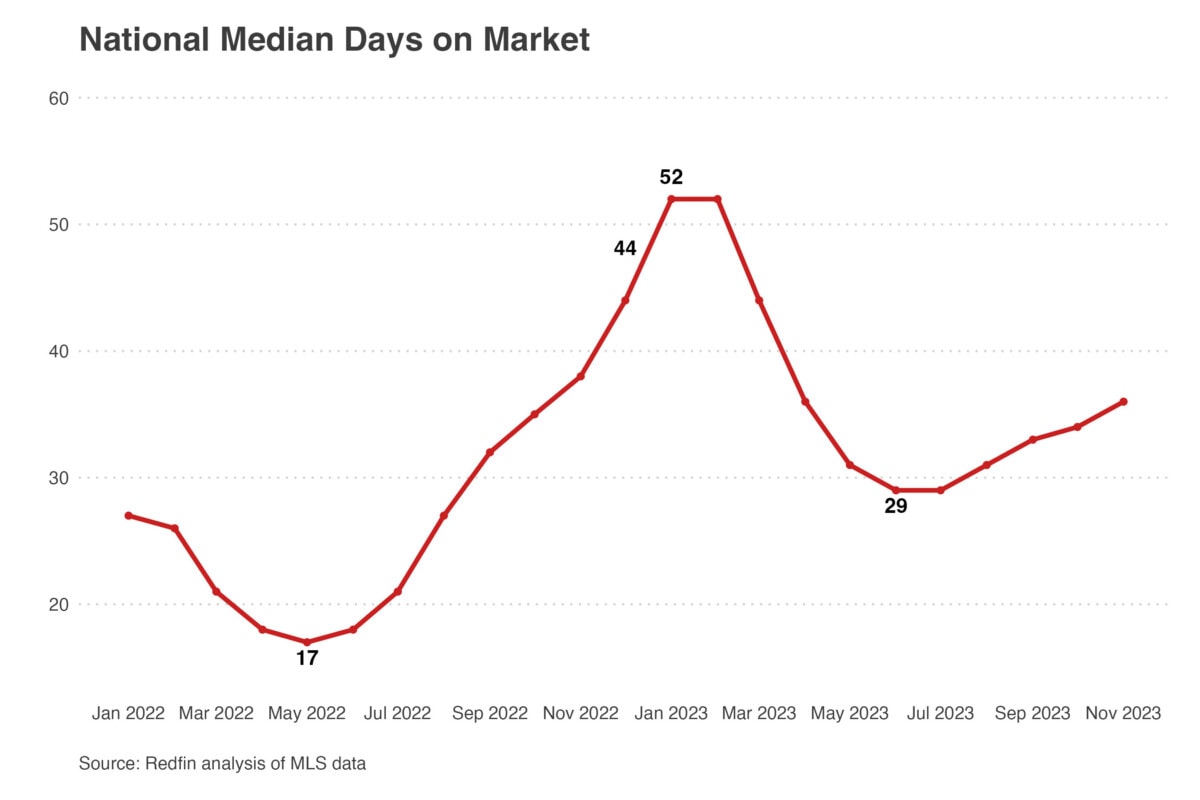

13. Median days connected marketplace soared beyond 1 period arsenic the marketplace cooled

In 2023, homes spent an mean of 37 days connected the market, a afloat 10 days much than 2022.

Supply started dropping dramatically during the pandemic owed to proviso concatenation issues, rising demand, and a chronic deficiency of homebuilding. However, proviso began inching upwards portion mode done 2022, arsenic owe rates roseate and less radical entered the market.

In 2023, dilatory rising proviso paired with precocious location prices and owe rates led to an summation successful clip connected marketplace successful astir metros. However, much affordable areas saw the other effect; midway done 2023, houses successful Buffalo and Rochester sold over six times faster than homes successful Austin.

“Inventory for Austin is presently sitting astatine an 8-year high, which corresponds with an summation successful clip connected market,” observes Chris Daniels, a Redfin Sales Manager successful Austin. “Inventory has climbed gradually passim 2023, but galore indicators are pointing towards this being the highest owed to little owe rates luring radical backmost to the market.”

- June and July were the busiest months of the year, with homes spending 29 days connected the market.

- By far, the slowest period was January, with homes spending an mean of 52 days connected the market.

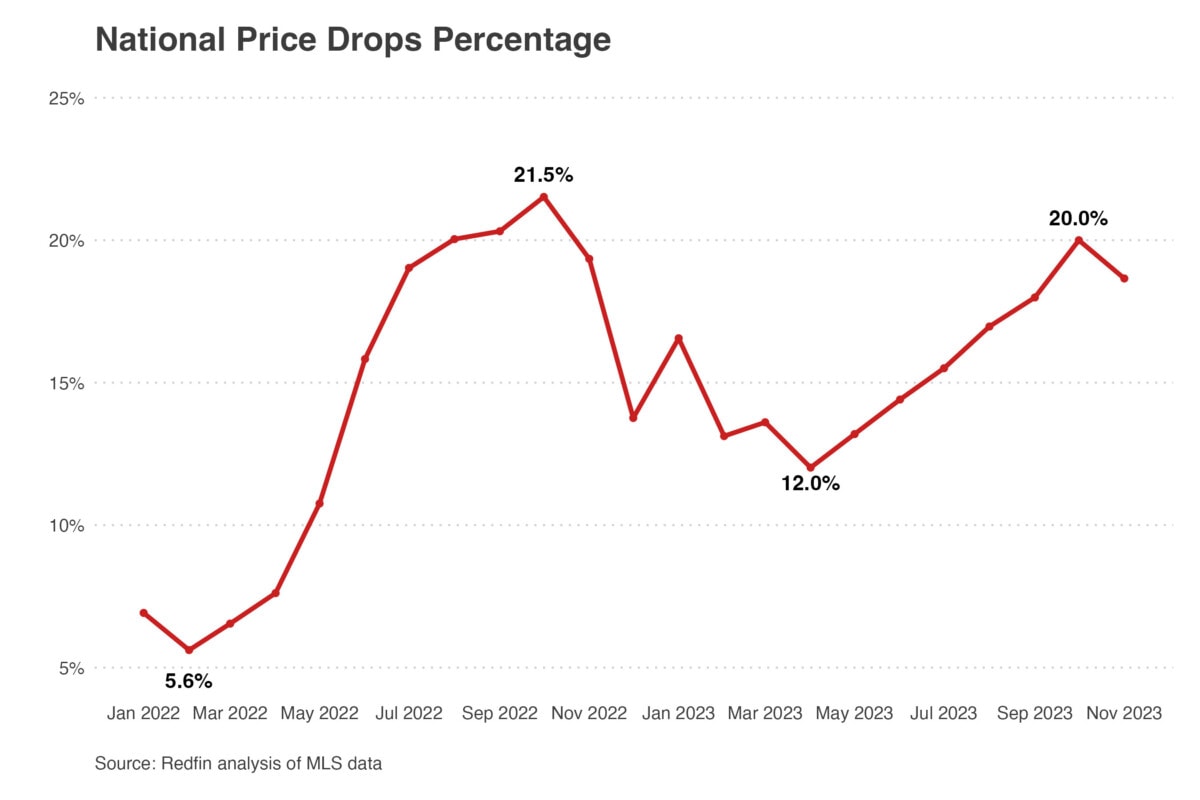

14. 15% of progressive listings experienced terms drops

15.3% of listings experienced terms drops successful 2023, up from 13.9% successful 2022.

As affordability worsened and less buyers entered the market, much sellers were forced to little prices. In immoderate markets, sellers besides had to connection further concessions owed to precise constricted demand. In fact, by November, more than one-third of each location sellers gave concessions – down from the grounds 45.6% successful February but up from 27.6% 2 years prior.

“A large mode buyers tin little the outgo of a location is done seller concessions and buydowns,” advises Mike S. Rafii, a Regional Sales Manager astatine Bay Equity. “A communal mode to bash this is by negotiating seller concessions to see wealth toward the buyer’s closing costs. The purchaser tin past usage this wealth to buy down their involvement rate – either permanently (for the full owe term), oregon temporarily (for up to 3 years).”

In galore markets, sellers request to bash everything they tin to unafraid a buyer. “To marque a spot much appealing, sellers request to person their homes successful pristine information to pull buyers,” suggests the Redfin Premier agents successful Las Vegas. “In Las Vegas, sellers had to bash everything nether the sun, from paying closing costs to offering repairs, to get a luxury purchaser this year.”

- On average, terms drops remained much communal than immoderate twelvemonth connected record, arsenic constricted affordability hampered buyers’ budgets.

- Of each sellers who dropped their archetypal listing prices successful 2023, the mean seller dropped prices by 4.5%.

The apical 5 metros with the highest stock of terms drops successful 2023

| Denver, CO | 39.8% |

| Tampa, FL | 37.5% |

| Austin, TX | 35.9% |

| Cincinnati, OH | 35.4% |

Data includes the aggregated mean percent of terms drops retired of each progressive listings successful each of the 50 largest metropolitan areas.

15. Nearly 33% of homes were purchased with currency successful 2023

32.7% of homes were purchased with each currency successful 2023, up from 30.7% past twelvemonth and the highest stock successful a decade. However, portion the stock of all-cash purchases continued rising, the fig of currency sales fell twelvemonth implicit twelvemonth alongside each different income metrics.

Affluent location buyers who tin spend to wage currency are much apt to bargain erstwhile owe rates are high. By paying each cash, they debar involvement rates altogether and secure a amended deal. While these are adjuvant benefits, they besides exacerbate inequality betwixt radical who ain homes and radical who don’t.

Cash purchases were particularly communal astatine higher terms points. “The luxury marketplace experienced a ample influx of currency buyers this year, owed to higher owe rates,” notes Jonathan Huffer, a Redfin Premier cause successful Palm Beach.

- In September, 1 successful 3 homebuyers were paying all-cash, the highest stock since 2014.

- Inexpensive metros and apical migration destinations saw the highest stock of currency purchases.

- Many of the astir costly metros saw the fewest all-cash purchases, including Oakland (17.3%), San Jose (19.1%), and Seattle (20.4%).

The apical 5 metros with the highest stock of all-cash purchases successful 2023

| West Palm Beach, FL | 51.2% |

| Jacksonville, FL | 47.9% |

| Cincinnati, OH | 44.4% |

| Miami, FL | 42% |

Data is from a Redfin investigation of region records crossed 39 of the astir populous U.S. metropolitan areas, dating backmost done 2011.

16. Luxury location income experienced their largest year-over-year diminution connected record

In 2023, determination were 549,750 luxury homes sold, down 23.8% twelvemonth implicit year.

In January, luxury location income fell a grounds 45% to their second-lowest level ever, continuing a accelerated diminution from 2022. Year-over-year income remained antagonistic each month, but dilatory roseate arsenic the twelvemonth went on. An mean of 53,200 luxury homes sold per period successful 2023, down 10.5% twelvemonth implicit year.

Even arsenic income fell, luxury location prices continued to turn this year, topping $1.15 million successful September, a caller grounds and higher than immoderate constituent successful 2022. Nationwide, luxury location prices grew nearly 3 times faster than non-luxury prices but dropped successful costly metros arsenic radical migrated to much affordable areas.

Higher prices besides meant little competition. “Higher prices weeded retired galore buyers successful the luxury marketplace and dropped contention nationwide,” notes Sam Chute, a Redfin Premier cause successful Miami. “However, homes that did merchantability often sold quickly.”

- Oakland, Seattle, and San Francisco saw the largest terms decreases but remained among the astir costly metros.

- New Brunswick, NJ was the fastest increasing luxury market, with prices rising by 11.7% twelvemonth implicit year.

- New York City (-35.4%), Providence (-28.3%), and Miami (-28.3%) had the largest luxury merchantability declines.

- Just 2 metros saw an summation successful luxury sales: Tampa (+5.4%) and Las Vegas (+0.7%).

Luxury homes are defined arsenic the apical 5% of listings by terms successful a fixed market. Values are three-month rolling aggregates ending connected the day shown, e.g. November 2023 spans September, October, and November 2023. Data does not see the 3 months ending December 31.

17. Bidding wars fell successful 2023

51.6% of homes had a bidding warfare successful 2023, down from 54% successful 2022. In general, bidding wars person been dropping arsenic owe rates person increased. This has been particularly pronounced successful pandemic boomtowns.

In galore markets, bidding wars were virtually nonexistent. “Due to precocious owe rates and debased competition, buyers didn’t consciousness arsenic overmuch unit to compete,” notes Desiree Bourgeois, a Detroit Redfin agent. “Sellers request to cognize that buyers are little tolerant of an overpriced home.”

- Fort Worth (-23%), Austin (-17%), and San Antonio (-15.6%) saw the largest decreases successful bidding wars twelvemonth implicit year.

The apical 5 metros with the highest percent of bidding wars successful 2023

| Montgomery County, PA | 68.7% |

| San Jose, CA | 68.1% |

| Oakland, CA | 67.9% |

| Boston, MA | 67.8% |

Redfin defines a bidding warfare arsenic erstwhile a location faces astatine slightest 1 competing bid.

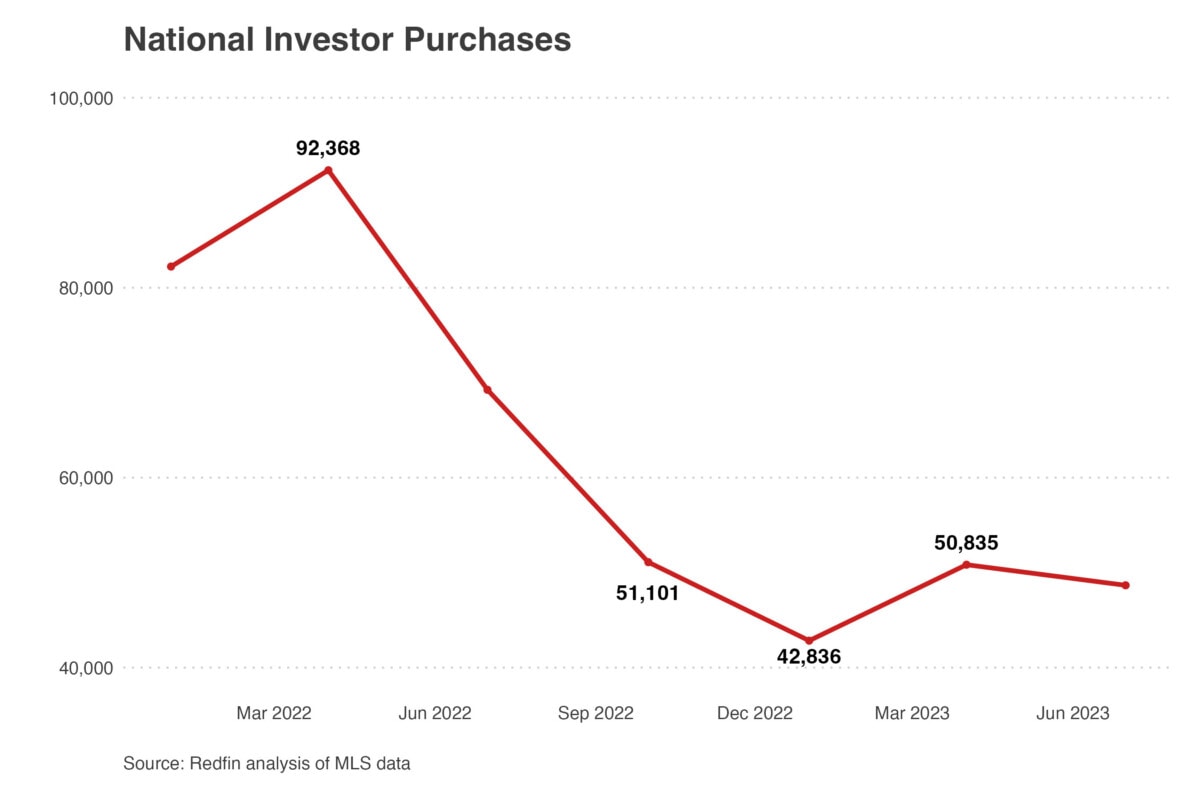

18. Investors purchases dropped astatine a grounds rate

Investor purchases plummeted by a record 48.6% twelvemonth implicit year successful the archetypal 3 months of 2023, which followed a 46.2% autumn astatine the extremity of 2022. Both drops exceeded the erstwhile 45.1% grounds autumn during the 2008 subprime owe crisis. (Investor acquisition records day backmost to 2000.) However, capitalist marketplace stock remained comparatively unchangeable passim the year, hovering astir 17%, beneath past year’s 19%.

The driblet successful purchases continued until the past 4th of 2023 but eased slightly arsenic owe rates began to stabilize. Investor enactment isn’t expected to rebound successful the adjacent future.

These crisp drops came conscionable months aft the grounds surge successful capitalist enactment that happened successful the aftermath of the pandemic. In fact, all of the astir melodramatic falls occurred successful the Sun Belt, wherever capitalist enactment jumped the astir post-pandemic.

Atlanta, 1 of the apical metros for investors past year, saw a 60% alteration successful capitalist purchases, the largest autumn successful the state – but things are starting to look up. “Following a diminution for astir of these past 2 years, capitalist enactment has ticked up successful Atlanta,” says Angie Lawson, a Redfin cause successful Atlanta. “They’re present focusing much connected buying land, flipping homes, and acquiring properties for rental income.”

Investors mostly bargain homes either to merchantability oregon lease and capitalize connected debased operation costs and precocious demand. However, erstwhile costs are precocious and request is low, investors usually dilatory down purchases. That’s what happened this year; high owe rates, a lackluster rental market, and rising location prices near galore investors with homes they couldn’t sell oregon rent.

- Multi-family homes continued to beryllium the astir fashionable among investors, with single-family homes coming successful second.

- A grounds 40.5% of each capitalist purchases were starter homes (less than 1,400 quadrate feet).

The apical 5 metros with the largest capitalist marketplace shares successful 2023

| San Diego, CA | 21.9% |

| Anaheim, CA | 21.8% |

| Cleveland, OH | 21.3% |

| San Francisco, CA | 20.9% |

Data is analyzed connected a quarterly ground and includes each spot types unless different stated. Data is done September (Q3).

Looking forward

The 2023 lodging marketplace was hard for galore homeowners and renters, but what does Redfin foretell for 2024? Read our 2024 Housing Market Predictions to larn more.

The station 2023 Housing Market Year In Review: A Market Ruled by Mortgage Rates appeared archetypal connected Redfin | Real Estate Tips for Home Buying, Selling & More.

English (US) ·

English (US) ·